{kind=link}

In the previous post, we started a series entitled EU 2024-2029: Forging a competitive path, in which we will analyse Telefónica’s vision on how to strengthen competitiveness and better position the European Union’s society and economy on the global stage. This series coincides with the start of the institutional cycle that runs from 2024 to 2029, following the European Parliament elections. Competitiveness will undoubtedly be the central priority guiding the EU’s forthcoming policy and legislative initiatives during this period.

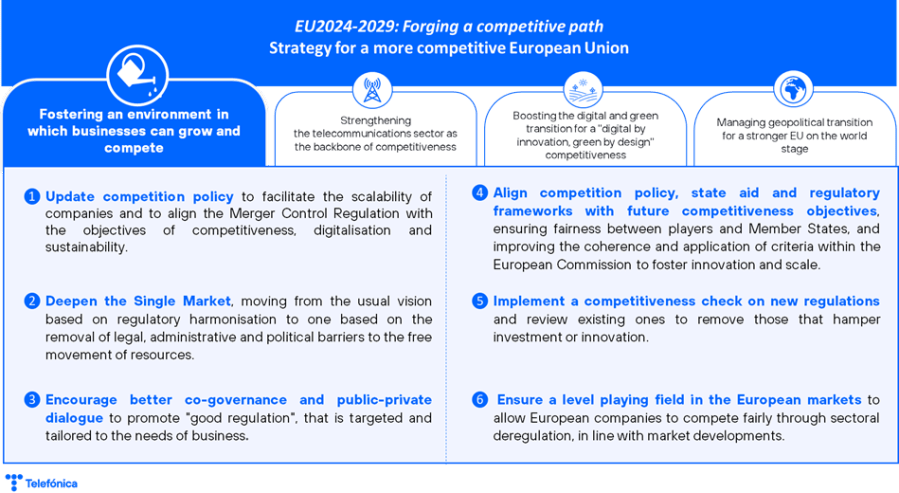

In this second post, we analyse the competitiveness strategy that Telefónica considers key and which it articulates in four axes. The first of these is the subject of this post and of crucial relevance for the success of the rest of the axes: the creation of a regulatory environment that allows European companies to grow and compete.

Regulatory tsunami and a complex framework?

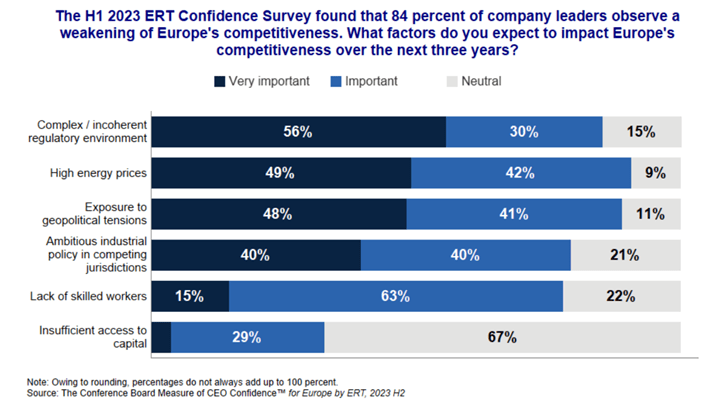

There is a general perception in the European private sector that a “regulatory tsunami” has become one of the main obstacles to their competitiveness over the last decade. This perception is supported by 86% of European Round Table (ERT) members, who argue that a complex, difficult to understand and inconsistent regulatory environment undermines the competitiveness of their companies.

To change this, we urge the next EC and EP to put the business case for EU industry and its competitiveness at the core of its actions. We need a clear and meaningful commitment that policymakers are determined to tackle this challenge head-on

There seems to be a misconception among policy makers that regulatory output or becoming the global prescriber of regulation, the so-called “Brussels effect”, gives European companies a competitive advantage.

However, excessive regulatory complexity results in administrative, legal and political barriers that make it difficult for companies to operate with agility and to take decisions on their development in the local or international market, with negative effects on their investment and innovation, as can also be observed in the telecommunications sector.

Thus, the existence of policies and regulations that are often not aligned or interpreted in the same way, not only hampers implementation, but also creates uncertainty and inequality between the different actors, and undermines the single market and hampers innovation.

For example, the ePrivacy regulation, which only applies to the telecoms sector, remains in place despite the enactment of the General Data Protection Act (GDPR), which establishes a general framework applicable to all sectors (including telecoms). In the areas of security, artificial intelligence and the digital market, the number of delegated acts and the interplay between regulations and implementing bodies are multiplying, often inconsistently with each other.

In Europe, companies have to devote significant resources to ensure compliance with complex, exhaustive and prescriptive regulations.

Consequences in terms of growth, prosperity and competitiveness

This situation is reflected in a gap of scale of European companies, whether in terms of revenue, size in terms of number of employees or geographical scope, vis-à-vis companies located in regions with more flexible and favourable regulatory frameworks for investment and innovation, which allow them to grow and compete.

In 2022, total market capitalisation in the US is 2.5 times larger than in Europe, and US companies are almost twice as large (by revenue). This gap reflects Europe’s lagging economic growth and prosperity, with implications for its future competitiveness and the sustainability of its social and economic model.

This gap in scale also extends to the field of innovation, where, for example, generative artificial intelligence (GenAI) promises to revolutionise societies and economies by significantly increasing productivity and fostering innovation at unprecedented levels. However, , according to McKinsey Global Institute, private investment in generative AI in Europe reached $1.7 billion in 2023, compared to $23 billion in the US, highlighting the lack of momentum in technological innovation.

Regulatory rigidity not only hampers innovation capacity in fields such as artificial intelligence (AI), leaving Europe behind competitors such as China and the US, but also increases the risk of relocation of investments and corporate decision-making centres. Companies seeking a more favourable and flexible environment for their operations, could relocate their activities outside the EU, with negative consequences for the region’s productive capacity, investment and strategic autonomy.

This risk has been highlighted by the implementation in the US of the Inflation Reduction Act (IRA), which offers benefits by simplifying and reducing the regulatory, tax and administrative burden on businesses. These policies attract businesses from around the world by creating an environment that promotes efficiency and cost reduction and creates a more favourable environment for investment and business growth.

In addition to the potential lack of competitiveness resulting from the regulatory framework, there is the challenge of globalisation and digitalisation. European companies face the challenge of losing market share and competitiveness, especially in the digital market, both globally and in their local markets due to competition from new international players, some of which are not subject to the same regulations as established companies.

Public policies to foster an enabling environment for competitiveness

It is therefore imperative that the EU transforms regulation from an obstacle into a competitive advantage, promoting a favourable environment for investment and innovation and strengthening the single market. This is necessary because without investment, innovation is not possible, and therefore competitiveness cannot be improved.

That is why Telefónica believes it is necessary:

- Update competition policy to facilitate the scalability of companies and align the Merger Control Regulation with competitiveness, digitalisation and sustainability objectives.

- Deepen the Single Market, evolving from the usual vision based on regulatory harmonisation to a vision based on the elimination of legal, administrative and political barriers to the free movement of resources.

- Encourage better co-governance and public-private dialogue to promote “good regulation”, that is targeted and tailored to the needs of business.

- Align competition policy, state aid and regulatory frameworks with future competitiveness objectives, ensuring fairness between players and Member States, and improving the coherence and application of criteria within the European Commission to foster innovation and scale.

- Implement a competitiveness check on new regulations and review existing ones to remove those that hamper investment or innovation.

- Ensure a level playing field in the European markets to allow European companies to compete fairly through sectoral deregulation, in line with market developments.

In the next post, we will examine the next strategic axis for a more competitive EU: how to reinforce the telecoms sector as the backbone of competitiveness in a global environment shaped by the digital economy.